The Rise of the Reallocation Economy: AI, Employment, and Structural Change

Jungmin Lee

Photo by iLixe48

The legendary investor behind the unparalleled success of the conglomerate holding company Berkshire Hathaway, Warren Buffett has built his investing empire thanks to his acumen for capturing the currents that drive the major changes responsible for transformations in the business world. His uncanny ability to ride the tides of such market changes endowed Buffett the famous sobriquet, the “Oracle of Omaha” (Schroeder, 2008). However, despite all this, he has not been shy about confessing the biggest investment mistake of his career: his decision to purchase Berkshire Hathaway itself. When Buffett acquired Berkshire in the 1950’s, the textile industry in the United States had already been in decline due to the cheap labor costs abroad. No longer was there much sense in manufacturing textiles, a highly labor-intensive field like agriculture and steelmaking, in the world’s most developed economy.

Not all gloom spells doom, however. The textile market in the U.S. has staged a surprising renaissance between 2009 and 2014, with exports growing by 45% to $18.3 billion. Today, the industry employs about 233,000 people, or 2% of the entire workforce in the country – a step down from the peak of 1.3 million in 1948, but impressive, nonetheless (DiLallo, 2015). What has driven this comeback? Is technology, often blamed for taking away people’s jobs, truly a job destroyer? What if technology leads to the creation of jobs as much as their demise?

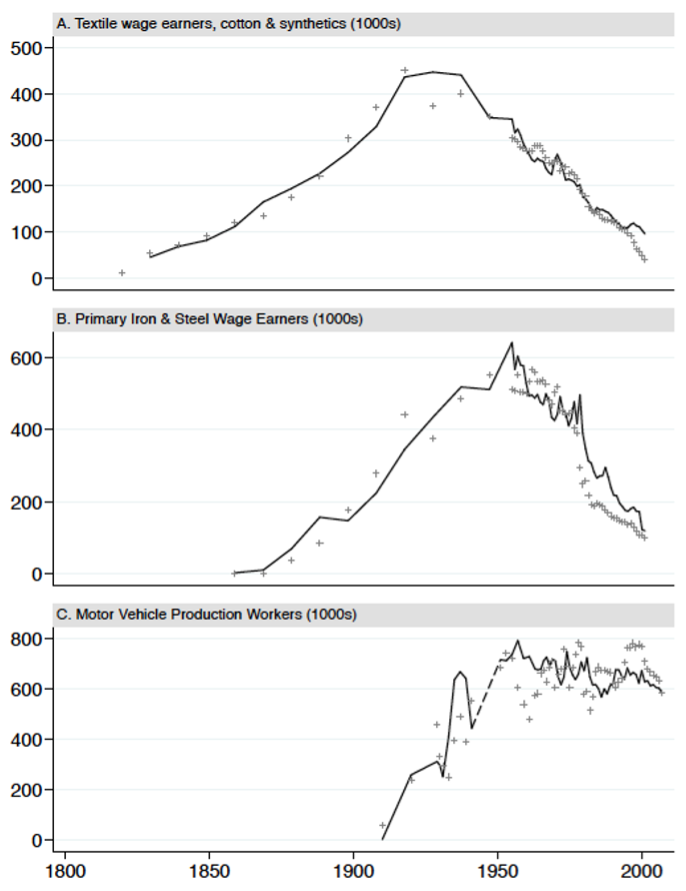

One group of economists and economic historians argue that technology has gradually driven the human labor force out of jobs. Indeed, the United States have witnessed the workforce in steel and textile industries shrink immensely: from over 500,000 to 100,000, and from over a million to 16,000 in 2011 (this is shortly before the above-mentioned period of resurgence). Much of this change owes to trade, frequently called offshoring; however, technology and offshoring are similar in that they both replace higher-paying positions with lower-paying ones as companies compete for lower prices and sometimes, higher quality per a unit of price paid by the consumer (Bessen, 2018).

In recent years, the advent of artificial intelligence, especially generative artificial intelligence (GAI), is projected to inflict further damage to this trend. As Korinek and Stiglitz (2019) stress, the “introduction of artificial intelligence (AI) is the continuation of a long process of automation.” Yet, the emergence of advanced AI technologies marks an inflection point in the general trend of labor force composition, affecting medium-to-high-skilled jobs (“white collar” jobs) as well as the unskilled ones (“blue collar” jobs) that have long been subject to de-industrialization. The change cannot simply be written off as alarmism: in general, unemployment depresses consumption, as “workers are also consumers, and they rely on their wages to purchase the products and services produced by the economy” (Ford, 2015). Machines, unlike those workers in the developing world during globalization who stand to benefit from the influx of manufacturing work, do not consume.

Still, the past trends do not necessarily indicate that developed economies have fallen into what seems like an inescapable recession: while they no longer grow at paces seen in rapidly industrializing nations such as China and India, their economies continue to post positive growth rates with healthy inflation (~2%). This can be attributed to the change in consumption patterns that occur in tandem with economic growth. In developing economies, the major share of national income is contributed by subsistence income; in other words, people live hand-to-mouth; however, as the economy grows, such income takes up a decreasing share of gross domestic product, accompanied by a rise in capital gains (Lewis, 1954). On the consumer side, this is consistent with Engel’s finding, which indicates that the share of spendings in basic necessities, such as food, to total income decreases with income growth.

The underlying mechanism behind economic growth under technological progress centers around productivity improvements. Buera and Kaboski (2009) suggest that productivity growth enabled by mechanization prompts “structural change along with constant growth rates of output and consumption.” Going back to our textile example, the rising productivity witnessed in textiles (and later steel and automobile manufacturing) has pushed down prices, which are attributed to the empowerment of the consumer. However, the consumer will not endlessly consume essentials such as bread and toothpaste just because prices drop; as Engel’s Law states, the share of necessities drop while the consumer looks to other goods and services with the larger purchasing power.

To examine the dynamics at play here, we can utilize the Cobb-Douglas production function (1928) to determine the relationship between production (Y), technological advancement (T), capital input (K), and labor input (L):

Y=T∙K^α∙L^((1-α) )

To determine production per unit of labor, we can divide both sides by L, obtaining the following.

Y/L=(T∙K^α∙L^((1-α) ))/L=T∙K^α∙L^(-α)

y=T∙k^α

Assuming a peak production level under the Neoclassical growth model, we can note an inverse correlation between technological advancement and capital input. The productivity improvements lead to higher capital stock and lower prices, resulting in expanded access to goods and services.

Given the above, labor and capital move away from sectors with high capital intensity to sectors with low capital intensity. (Acemoglu and Guerrieri, 2008) In other words, while sectors in the growth stage of the business cycle require the most capital to generate maximum output, this cannot go on indefinitely, and both output and employment decline. Such is the case with the United States, where the past half-century has seen employment and investments drop in manufacturing and rise in services: as the past capital deepening in the former has maximized productivity, this has incurred the unfortunate cost of divestment and job shrinkage. (Baumol, 1967; Rowthorn and Ramaswamy, 1999) As seen in the Cobb-Douglas production function, technological advances can offset capital intensity problematic in advanced economies and can combine with labor to return output to the equilibrium level while lending copious thrust to capital formation. (Matsuyama, 2009)

Most importantly, the synergistic relationship between productivity gains and expanding markets allow multiple industries to flourish, one by one, as seen in Figure 1. (Matsuyama, 2002) This is because the increasing capital stock and decreasing income flow into peak industries result in the capital being reallocated to other industries. A type of “balloon effect,” the growth of beneficiary industries will ironically lead to the growth of other fields, both conventional and novel. Applying this to the case of artificial intelligence, the lack of capital deepening in mature stages of AI-driven industries can enable the allocation of capital and labor towards a Pareto improvement—overall employment can suffer, but those employed enjoy stable and high incomes with lower barriers to entry, labor intensity, working environment and hours. (Korinek and Stiglitz, 2019)

As automation intensifies thanks to the rollout of artificial intelligence in many industries, employment losses are inevitable and unfortunate. The precise extent to which existing jobs will be removed, and by extension, how high the unemployment will be, is highly unclear and warrants further research. However, as happened with previous automation cycles, increased productivity can pave a way to new opportunities in the form of lower prices, higher quality of goods, and a wider availability of quality products and services. Even the most advanced economies are far from being full autarkies. With AI, which is said to have a substitution elasticity of >1, the sector rotation trend described earlier may not just end up benefiting existing sectors and industries but can lead to the creation of completely new industries. This, perhaps, is a more interesting issue to pursue—possibly inaugurating an entirely new field of economics.

Figure 1 Employment in Textile, Steel, and Auto Industries (Source: Bessen, 2018)

References

Acemoglu, D., & Guerrieri, V. (2008). Capital Deepening and Nonbalanced Economic Growth. Journal of Political Economy, 116(3), 467-498. DOI: 10.1086/589523.

Baumol, W. J. (1967). Macroeconomics of unbalanced growth: The anatomy of urban crisis. The American Economic Review, 57(3), 415-426.

Bessen, J. (2018). AI and Jobs: The Role of Demand. NBER Working Paper Series. NBER.

Buera, F. J., & Kaboski, J. P. (2009). Can Traditional Theories of Structural Change Fit the Data? Journal of the European Economic Association, 7, 469-477. https://doi.org/10.1162/JEEA.2009.7.2-3.469

Cobb, C. W., & Douglas, P. H. (1928). A Theory of Production. American Economic Review, 18(Supplement), 139–165. Retrieved from https://www.jstor.org/stable/1811556

DiLallo, M. (2015, October 3). The Textile Industry Has Changed a Lot Since Warren Buffett's Big Mistake. The Motley Fool. Retrieved from https://www.fool.com/investing/general/2015/10/03/textile-industry-has-changed-a-lot-since-warren-bu.aspx

Engel, Ernst (1857). "Die Productions- und Consumtionsverhältnisse des Königreichs Sachsen". Zeitschrift des statistischen Bureaus des Königlich Sächsischen Ministerium des Inneren. 8–9: 28–29. ... je aermer eine Familie ist, einen desto groesseren Antheil von der Gesamtausgabe muss zur Beschaffung der Nahrung aufgewendet werden ...

Korinek, A., & Stiglitz, J. E. (2017). Artificial Intelligence and Its Implications for Income Distribution and Unemployment. NBER Working Paper Series. NBER

Lewis, W. A. (1954). Economic Development with Unlimited Supplies of Labour. The Manchester School, 22(2), 139-191. Retrieved from https://doi.org/10.1111/j.1467-9957.1954.tb00021.x

Matsuyama, K. (2009). Structural change in an interdependent world: A global view of manufacturing decline. Journal of the European Economic Association, 7(2‐3), 478-486.

Matsuyama, K. (1992). Agricultural productivity, comparative advantage, and economic growth. Journal of Economic Theory, 58(2), 317-334.

Rowthorn, R., & Ramaswamy, R. (1999). Growth, Trade, and Deindustrialization. IMF Staff Papers. 46(1), 18-41.

Schroeder, A. (2008). The Snowball: Warren Buffett and the Business of Life. Bantam Books.